A tale of two tokens: Introducing Tin & Drop, our two Investment Tokens

This article is the first of a series explaining in depth our upcoming release of Tinlake and how it fits into the DeFi ecosystem on Ethereum.

Today we dive into a feature of the Tinlake smart contracts to showcase how lenders can invest in Tinlake loans.

Tinlake is Centrifuge’s smart contract framework for bundling loans collateralized by NFTs. It allows investors to invest in these portfolios of loans by issuing and selling ERC20 tokens that represent a claim on value generated by the loan portfolios through interest accumulation, loan repayments and potential liquidations.

We’ve used Tinlake for a first set of transactions to finance — among others — music royalty payments and real estate with Maker. Using the Tinlake smart contracts, Lendflo is factoring SME receivables in the UK to bring transparency to borrowers and build a worldwide network of buyer-supplier relationships you can trust.

Some people have a different appetite for risk: senior/junior tranches in structured finance

Investors often want different kinds of risk exposure and yield on the same asset class. In the traditional finance world one way to achieve this is by using structured finance products and introducing a two tiered investment structure. Investors can invest in two classes of shares where one is a high risk but high yield class. The second class of shares has a lower yield but is protected from losses by the first class of shares. In finance this is usually called an A/B tranche or junior/senior tranche structure.

To illustrate how this works, let’s look at a hypothetical $1M fund investing in SME invoices targeting an average annual interest rate of 9%. When setting up a structured fund, part of the paperwork is to define how many shares are being issued in each class. For example the issuer could say they will sell 20% of the $1M investment in a junior tranche and 80% in a senior tranche. Let’s assume the senior tranche is guaranteed a fixed return of 5%. The junior tranche has a variable return depending on the success of the investment.

Now let’s look at a few different scenarios to explain how this structure affects the risk and return of the different investment classes.

The Base Case Scenario

Assume that the money to return to investors is $1.09M based on the 9% interest rate ($1M in principal and $90k in interest). During the lifetime of the fund, any repayments are first used to repay the share of the senior investors along with the 5% interest accrued on their investment (5% of $800k = $40k). Once all outstanding senior debt and interest has been paid off, the waterfall pays out the remaining proceeds to the junior investors. That means that if there are no losses, the junior investors will be paid $50k on a $200k investment. This is equivalent to a 25% return.

Partial Loss for the Junior Tranche

Let’s assume again that out of the $1M lent, $1.09M were due incl. accrued interest. However there is a 6% default rate resulting in a total loss of $60k of the portfolio. For simplicity, we further assume that interest is impacted similarly, so the total interest paid from the portfolio is $84.6k. The senior tranche is not impacted and still returns 5% of $800k equal to $40k. The junior investors take the first loss and their net value drops to $140k. The junior tranche still receives the remaining interest payments of $44.6k from the waterfall. Thus, overall the junior tranche has an ending net value of $188.6k equal to a loss of 7.7%.

Maximum level of protection for the senior tranche

The senior tranche would be protected against any losses of their investment and their guaranteed fixed return as long as potential defaults do not exceed the volume of the junior tranche. This would be the case up to a default rate of 22.9% under the above assumptions. With a default rate of 22.9% the loss of the portfolio is $229k leaving a total of $771k of the loan portfolio being paid back. The total interest still paid from the portfolio is $69k. Thus, the senior tranche is not impacted, receiving $840k ($771k + $69k) and still returns 5%. The junior tranche takes the first loss again and their net value drops to $0k. For defaults higher than 22.9% the senior tranche would also start to accrue losses, first on their expected return, and then on their initial investment.

Tinlake’s two investment tokens: Tin and Drop

Tinlake implements this functionality by issuing two tokens, the Tin and Drop tokens. These two tokens behave very similarly to how tranches are modeled in the traditional finance world. The Tin token can be seen as the junior tranche and token holders that own these tokens take second priority to the Drop token holders when money flows from borrowers back to funders, but depending on the performance of the pool also have the potential to generate a much higher return on their token value than Drop token holders.

Implementing these two tranches in code makes them first class citizens of the DeFi ecosystem and thus a much more powerful tool.

How Tinlake models investors claims and the flow of funds

Tinlake is built to support a variety of different setups and is highly customizable. One of the aspects that can be customized is how the investor tokens are configured. Tinlake can be configured with two investor tokens (Tin & Drop) to support a two tranche system. If the portfolio should be set up without this structure it can be deployed with just one (Tin).

Minimum Tranche Ratio

A Drop purchaser taking the senior tranche would want to have a guarantee that there is at least a minimum percentage of Tin in the pool to make sure that they are protected against a certain amount of losses. Setting this variable guarantees them a certain risk profile. When deploying a pool this variable needs to be set and enforced by the contracts. When the minimum ratio is broken, investments and the issuance of additional Drop token is stopped until the minimum ratio is restored.

Interest Rate Model

The Drop token’s return is defined by a fee function. Our default implementation let’s the deployer set an interest rate compounding per second on the deployed capital but one could also quite easily peg it to say Maker’s stability fee or any other externally defined fee function.

The Tin token only gets a return on their investment if the Drop token holders have all been fully redeemed. Therefore, Tin token holders do not have a guaranteed fee or return but measure their return by what the Drop token contract determines to be the appropriate return.

Tranches on steroids

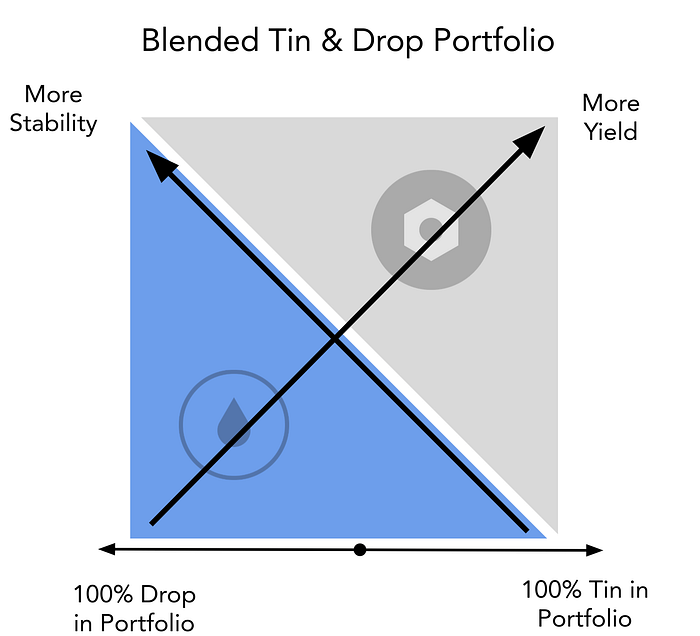

The distinction between investing in Tin or Drop gives investors two different choices in terms of risk and return profile — one rather stable and safe, but lower yielding token and offering a higher risk but also potentially higher returns. However, investors are not bound to only invest in one of the tokens. By allocating their investment across both tokens they can create their individual risk/return profile, that caters to their specific risk/return appetite.

Using smart contracts to codify these two behaviors and implement the tranches does not only guarantee that the system will behave the way it is expected at all times but it also comes with a huge amount of flexibility. Investors can allocate their investment between the two tranches on a sliding scale adjusting their own risk exposure on demand.

Tin + Drop + MakerDAO = ❤️

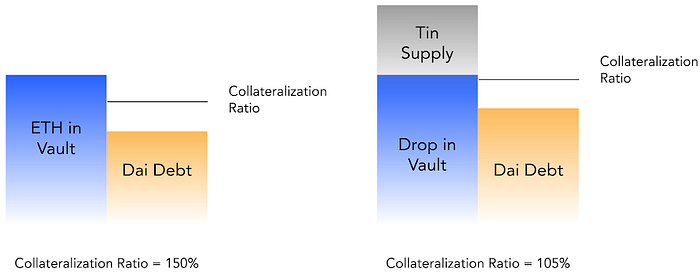

In the context of DeFi our two tokens open up a wide range of options for leveraging these two different kinds of assets. Let’s take MakerDAO as an example. People often call Maker the central bank of crypto. They have an appetite for large amounts of collateral but want these assets to be as low risk as possible. Maker is the ideal candidate to invest the Drop token. Let’s look at how asset originators can use their loans on MakerDAO as collateral.

An asset originator (such as an invoice factoring business) can configure their Tinlake portfolio with a junior tranche and fund part of that tranche. They can work with investors who know their particular asset class and have an appetite for leveraged exposure through the Tin token to their risk. Knowing these assets extremely well and having a very good idea about their risk, they have the confidence to put up some initial capital but lack the financial resources to scale it. Having set up the Tin tranche they can now turn to Maker for leverage, offering a chance to approve the Drop token as collateral on MCD, while guaranteeing that MKR holders are only affected if default losses exceed Tin’s allocation.

In this scenario, the question MKR holders have to ask themselves is not anymore: what’s the risk of even a miniscule amount of losses in this large diversified portfolio of loans? But rather, do we believe that this portfolio is going to have a default rate of less than X%?

Lowering the collateralization ratio

Conversely, the two token setup which makes the value of the Drop token extremely stable could also push the collateralization ratio that MCD could accept into much lower numbers. The reason for that is that by investing in the Drop token, to use our example from above, Maker gets a portfolio of loans worth $1.09M to back a debt in Drop token of only $840k. Part of the equation for MCD is not just what their investment is and the possible return but also how much “insurance” in form of Tin investment is available. The MKR governance community can thus give a much lower collateralization ratio and still be well protected.

Learn more? Get a preview on the Tinlake contracts

If you like what you’ve heard and want to learn more about how we’ve built the contracts and how Tinlake works in detail, I’m hosting a community call on the the contract internals for both technical and non technical folks to learn more on Feb 25th at 9am PST/6pm CET.

Stay tuned for more on the upcoming release of Tinlake.

Want to learn more? Follow us on Twitter / Read more on Medium / Check out our website / Or join us, we are hiring!

Thanks Dennis, Charly, Jason for your edits and contributions!